One of the most common financial goals that we come across in financial plans that we do for families, is the need to have the finances well prepared for education needs – both at school levels and at college levels. As parents who have their children going through their college education currently, both Shalini and myself have had a chance to discuss and reflect on this over the years, as education has tended to be one of the most critical goals for most families.

Education costs have surged both domestically and globally, rising far faster than inflation or income growth for most households. What was once a manageable household expense has become a powerful, silent drag on long-term wealth accumulation even for those who can “afford” premium schools but often underestimate the opportunity cost.

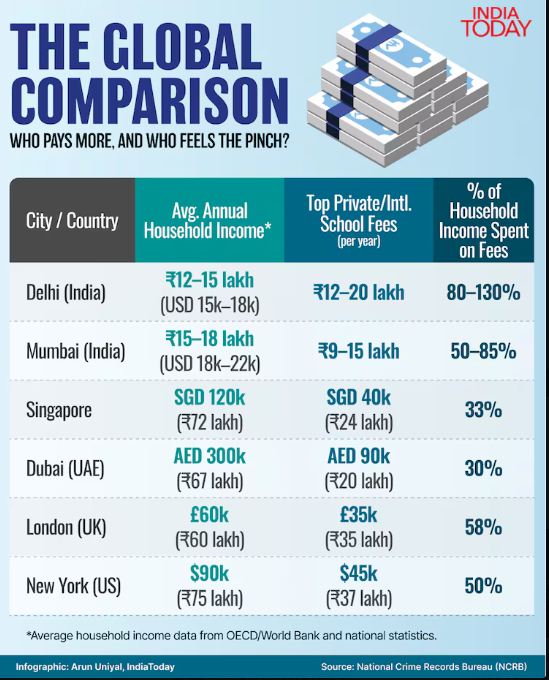

The Global and Indian Tuition Spiral

In India, private school and college fees have jumped 150–200% in the past decade, while incomes have grown about 60–70% on an average. Urban parents now spend up to 20 lakh a year per child – numbers that were once associated with Ivy League tuition. Top boarding schools can charge up to ₹30 lakh annually.

The more one earns, the more one tends to spend on “premium” education – international schools, global universities and enrichment programs. A family with children might easily pay ₹15 – 25 lakhs a year in domestic tuition fees and ₹80 lakhs- 1 crore overseas – essentially funding a multi-crore transfer of private wealth to the education sector over two decades.

When Prestige Outweighs Potential

Having watched this closely over the years, we have concluded that expensive schooling doesn’t guarantee success. True achievement stems from curiosity, grit, and adaptability, not the size of the fee paid. Many parents’ mistake brand prestige for quality, overlooking their child’s real potential.

Regardless of whether students attend elite or average schools, the competition for top institutions like IITs, IIMs, Harvard, and Oxford remains as intense as ever. High tuition may refine resumes, but it doesn’t guarantee entry or success. The real investment lies in nurturing a child’s skills, curiosity, and resilience — not in paying for prestige

International Education Amid Global Uncertainty

For students in IB or Cambridge boards, shifting back to India for higher studies can be tough. The NCERT-based entrance exams like JEE, NEET, and CUET demand rote preparation, unlike the conceptual focus of international programs.

At the same time, global uncertainties from visa restrictions to rising foreign tuition fees and geopolitical risks are making overseas education less predictable. In short, international schooling works best when there’s a clear, well-planned path abroad, and is not just as a lifestyle choice.

The Reverse Compounding Effect

Every rupee spent on education is one not invested elsewhere. A family that spends ₹50 lakh–₹1 crore per child from nursery to college effectively sacrifices ₹2 crore for two children. Had this been invested at a modest 10% p.a. annual return, it could have multiplied in 15–20 years — enough to start a business or create a retirement corpus.

Education costs should ideally stay below 15–20% of annual income; beyond that, they crowd out investments, emergency funds, and wealth-building opportunities.

Of course, there will always be a cost for an education, but should it be as high as it is for many families in light of their family balance sheet and profit and loss statement is something to be thought about?.

Lifestyle Inflation

The drain isn’t limited to tuition. High-fee schools often trigger lifestyle inflation with better phones, cars, parties, holidays so that children “fit in.” Cash flow that could fund long-term assets instead sustains social parity. Some parents even borrow or redeem investments, unknowingly risking their financial stability for short-term prestige. Be sure that you can afford the education without compromising on other important short term and long term goals that your family may have.

Smart Planning for Wealth and Education

- Leveraging Digital Tools for Learning – Students today have unmatched access to world-class learning online from Ivy League lectures and Coursera masterclasses to AI tutors like ChatGPT. Digital platforms are democratizing education, offering top-tier content without premium fees, while AI personalizes and simplifies learning, narrowing the gap between elite campuses and online classrooms

- Manage Costs Realistically – Premium schools require disciplined investing; avoid letting education consume more than a fifth of your income.

- Prioritize Value Over Vanity – Select schools that align with your child’s aptitude, not just prestige. True success is driven by capability, not price tags.

- Plan multi-generationally – Education should empower without eroding family capital. Balance emotional aspirations with long-term financial prudence.

- Teach Financial Awareness – Introduce children early to budgeting, saving, and investing lessons, probably as valuable or maybe more than any school brand.

- Diversify Globally – If you can afford an international education, invest at least partly in global markets, precious metals, and USD-denominated assets to hedge against rupee depreciation, and build a partial non INR corpus for future education.

Disclaimers

- Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

- Registration granted by SEBI, membership of BASL and certification from National Institute of Securities Markets (NISM) in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

- The information is only for consumption by the client and such material should not be redistributed.

- The securities quoted are for illustration only and are not recommendatory.

- Past performance is not an indicator of future performance.

- Please consult your investment advisor before investing.

- This material is for information and educational purposes only.

- Details are at https://planahead.in/disclaimers-disclosures/.