As wealth grows, the number of moving parts often grows with it. A family may start with a few mutual funds, fixed deposits, and insurance policies. Over time, this can expand into direct equity, PMS, AIFs, bonds, real estate, ESOPs, offshore investments, private deals, loans, trusts, wills, tax filings, and multiple family members with different goals.

The challenge is not that wealth has become large. The challenge is that the systems around the wealth may not have grown at the same pace.

For Investors, the important message is to understand that complex wealth does not have to create operational confusion if it is supported by clear structures.

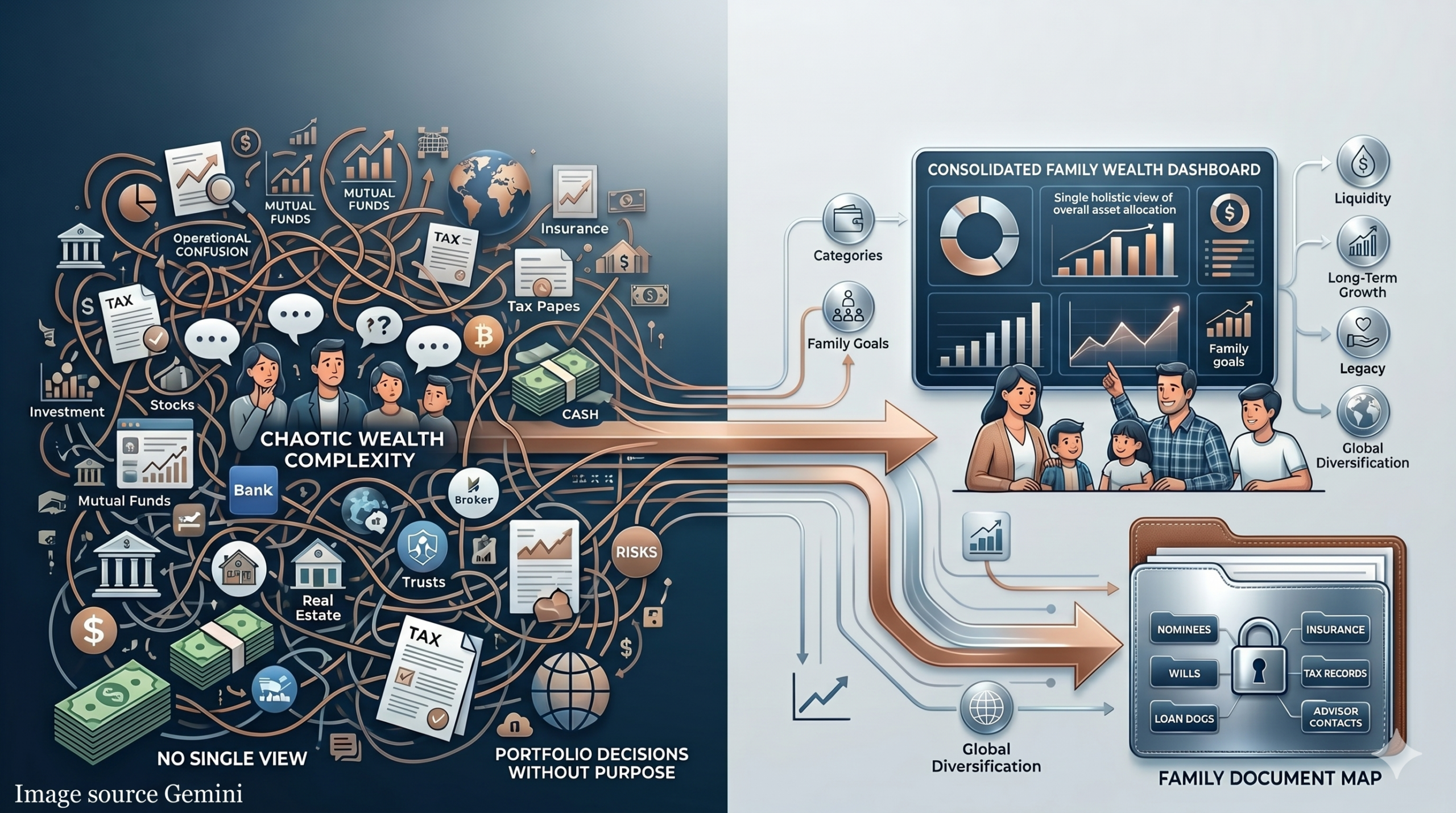

- Too Many Investments, No Single View

Many families hold investments across multiple banks, brokers, platforms, and advisors. Each report may look correct individually, but the family may still not know the overall asset allocation, total equity exposure, debt maturity profile, liquidity position, or concentration risk.

One action an investor can take for this issue is to create a consolidated family wealth dashboard. This should show the full picture across asset classes, entities, and family members. Without this, decisions may be made based on fragments rather than the total portfolio.

This will also provide key insights into the family’s overall wealth and help them move forward with a holistic approach.

- Portfolio Decisions Without a Clear Purpose

A portfolio can become complicated when every investment is bought for a different reason—tax saving, past returns, a relationship recommendation, a market opportunity, or a short-term idea. Over time, the portfolio may become active, but not necessarily purposeful.

Link investments to clear buckets and goals: liquidity, income, long-term growth, legacy, philanthropy, business reserves, or global diversification. This makes portfolio reviews sharper and reduces unnecessary overlap.

This also helps investors stick to a plan. For example, if investors associate a particular savings or investment with retirement rather than clubbing it with other investments, it is more likely that the retirement investment will follow through as per plan and without any major diversion.

- Documentation Becomes a Hidden Risk

Operational risk is often thought of as a boring topic, but in it lies important areas: nominee details, joint holdings, bank mandates, demat access, insurance records, loan documents, property papers, and tax reports. These are rarely discussed in market commentary, but they can create serious stress during emergencies or succession events.

Maintaining a family document map will be a key aspect of this problem. It should be clearly mentioned what exists, where it is stored, who has access, and when it was last updated.

This file can include details such as:

- Investment account numbers and platform details

- Nominee and joint-holder information

- Insurance policies and maturity dates

- Loan and liability details

- Property documents and ownership records

- Tax records and capital gains statements

- Will, trust, and succession-related documents

- Contact details of key advisors, bankers, tax advisors, and lawyers

The aim is not only to store documents, but to make sure that the family knows what exists, who owns it, who can access it, and what needs to be updated.

4. The Problem: Governance Is Informal Until It Is Tested

In many families, investment decisions are understood by one or two people. But when the next generation enters, or when wealth passes across branches of the family, informal understanding may not be enough.

The solution for this would be to define a decision rule. Who approves new investments? Who monitors risk? What happens if one family member needs liquidity? These questions are important to answer before a stressful situation arises, which can force an emotional or wrong decision.

The aim is not to make wealth management more complicated. The aim is the opposite: to make complex wealth easier to understand, monitor, and transfer.

The real value of structure is clarity. It helps ensure that wealth is not only invested well, but also organised well.

Disclaimers.

- Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

- Registration granted by SEBI, membership of BASL and certification from National Institute of Securities Markets (NISM) in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

- The information is only for consumption by the client and such material should not be redistributed.

- The securities quoted are for illustration only and are not recommendatory.

- Past performance is not an indicator of future performance.

- Please consult your investment advisor before investing.

- This material is for information and educational purposes only.

- Details are at https://planahead.in/disclaimers-disclosures/